Federal Deposit Insurance Corporation

Office of the Comptroller of the Currency

Office of Thrift Supervision

WASHINGTON--The quality of large syndicated bank loans showed marked improvement this year, according to the Shared National Credit (SNC)1 review released today by federal bank and thrift regulators. Adversely rated loans continue to subside, although certain industries continue to have a high concentration of adversely rated loans.

The results -- reported by the Board of Governors of the Federal Reserve System, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, and the Office of Thrift Supervision -- are based on analyses prepared in the second quarter of 2004 and reflect business and economic conditions at that time.

Total loan commitments2 classified as either substandard, doubtful or loss fell by $78.2 billion, or 51 percent, from the previous year, compared with a net decrease of $4.9 billion, or 3 percent, the year before. Commitments rated special mention decreased by $22.4 billion, or 41 percent, in contrast to 2003 when they fell by $23.8 billion, or 30 percent. None of these figures includes the effects of hedging or other techniques that organizations often employ to mitigate risk.

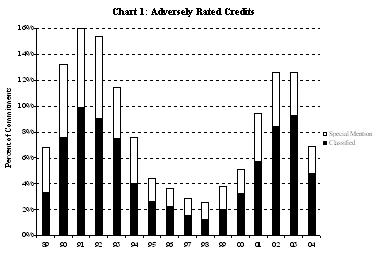

The ratio of classified loan commitments to total commitments fell to 4.8 percent, the lowest level since 2000, as industry charge-off trends and demand in the secondary market for lower quality assets removed many of the weakest loans from the banking system. Total adversely rated credits (classified and special mention combined) also fell considerably, to 6.9 percent of total commitments (see Chart 1 below).

Adversely rated credits (also known as criticized credits) are the total of loans classified substandard, doubtful, and loss--and loans rated special mention. Classified credits are only those rated substandard, doubtful, and loss. Under the agencies' Uniform Loan Classification Standards,3 classified loans have well-defined weaknesses, including default in some cases. Special mention loans exhibit potential weaknesses, which may result in further deterioration if left uncorrected.

Overview

In aggregate, the 2004 SNC Program covered 7,490 credits totaling $1.5 trillion in loan commitments to 4,746 borrowers. Total commitments were down by 6 percent from the prior year and down 25 percent from the 2001 peak of $2.0 trillion. This is consistent with market data pointing to lower customer demand, tighter underwriting standards, and attractive capital market financing alternatives. Total outstandings, or drawn amounts, were down 17 percent from the prior year to $500 billion.

For the 2004 review, total loan commitments classified as substandard fell $57 billion, or 51 percent from the prior year, while doubtful credits dropped by $16.8 billion or 57 percent (see Table 1 below). Commitments classified as loss fell $4.3 billion, down 40 percent from the prior year. Doubtful and loss amounts reflect the continued downward migration of credits with previously identified weakness. While total classified commitments fell sharply, the portion of outstanding nonaccrual4 classified loans fell at a slower rate (41 percent) to $30.1 billion.

Table 1 SNC Classifications ($ billions)

| Total Commitments | |||||

|---|---|---|---|---|---|

| % Change 2003 - 2004 |

2004 | 2003 | 2002 | 2001 | |

| Substandard | |

|

|

|

|

| Doubtful | |

|

|

|

|

| Loss | |

|

|

|

|

| Total Classified | |

|

|

|

|

| Percent of Commitments | |

|

|

|

|

| Memo: Nonaccrual classified | |

|

|

|

|

| Special Mention | |

|

|

|

|

| Total Criticized | |

|

|

|

|

| Percent of Commitments | |

|

|

|

|

| Total SNC Commitments | |

|

|

|

|

Industry Trends

The quality of the SNC portfolio improved markedly in all industries (see Appendix B).5 The strongest improvement occurred in the Manufacturing sector, with a $23 billion, or 54 percent, decline in classified commitments. Classified credits in the Oil, Gas, Pipelines and Utilities segment fell $13.9 billion, but remained at significantly elevated levels, with 13.8 percent of commitments classified. The Telecommunications and Cable segment also exhibited improvement, although exposure to previously identified weaknesses still linger. Well-documented problems facing airlines continue to drive classifications in the Lodging and Transportation segment. Other segments such as Financial Services and Insurance and Construction and Real Estate showed modest classification rates that were below those for the entire SNC program. Credits identified for special mention fell by $22.4 billion with strong declines experienced in every industry except Telecommunications and Cable. These declines were driven by a migration of a portion of prior year special mention credits to classified categories, as well as a decline in newly identified credits with potential weaknesses. Of total losses in 2004, $3.6 billion, or 56 percent, were directly attributable to the weakened Energy sector, most of which is related to outcomes of bankruptcy filings. The remaining losses were spread widely across a variety of industries.

Trends by Entity Type

During 2004, the share of SNC commitments held by U.S. banks and nonbank entities6 each edged up 1 percentage point to 46 percent and 12 percent, respectively. The share held by foreign banking organizations (FBOs) continued to decline, totaling 42 percent in 2004 (see Table 2). All types of lenders experienced a decline in classified assets during 2004, with U.S. banks showing the largest improvement, down 57 percent from the prior year. The quality of holdings also varied among entity types, with classifieds amounting to 3 percent of total commitments at U.S. banks, compared with 5 percent at FBOs and 13 percent at nonbanks. Total nonaccrual outstandings improved for all entity types. Most notably, U.S. banks experienced a 57 percent decline.

Table 2 Exposures by Entity Type

|

|

2004 |

2003 |

2002 |

2001 |

|---|---|---|---|---|

| Share of Total Commitments |

||||

| U.S. Banks |

46% |

45% |

45% |

46% |

| FBOs |

42% |

44% |

45% |

46% |

| Nonbanks |

12% |

11% |

10% |

8% |

| Total Classifications ($ Billions) |

||||

| U.S. Banks |

18.8 |

43.6 |

54.4 |

48.6 |

| FBOs |

31.3 |

65.0 |

61.7 |

44.2 |

| Nonbanks |

23.9 |

43.6 |

41.1 |

24.5 |

| Totals |

74.0 |

152.2 |

157.1 |

117.3 |

| Total Classifications (% Increase) |

||||

| U.S. Banks |

-56.8% |

-20.0% |

11.8% |

85.5% |

| FBOs |

-51.8% |

5.5% |

39.2% |

99.4% |

| Nonbanks |

-45.3% |

6.2% |

67.9% |

76.0% |

| Totals |

-51.4% |

-3.2% |

33.8% |

88.3% |

| Classifieds as % of Commitments |

||||

| U.S. Banks |

2.6% |

5.8% |

6.4% |

5.1% |

| FBOs |

4.9% |

9.0% |

7.3% |

4.7% |

| Nonbanks |

12.9% |

24.4% |

23.0% |

14.6% |

| Totals |

4.8% |

9.3% |

8.4% |

5.7% |

| Total NonAccrual Outstanding ($ Billions) |

||||

| U.S. Banks |

5.7 |

13.3 |

15.5 |

n.a. |

| FBOs |

13.4 |

22.8 |

19.8 |

n.a. |

| Nonbanks |

11.0 |

15.0 |

15.7 |

n.a. |

| Totals |

30.1 |

51.0 |

51.0 |

n.a. |

Risk Management by Banks

Banking organizations remain vigilant in identifying problem credits and have generally reflected the appropriate risk rating in their internal ratings of credits in the SNC program. Although credit quality has improved, banking organizations must continue to carefully monitor the condition of their borrowers to ensure that they promptly identify and address any emerging weaknesses and adjust loan loss allowance levels appropriately.7

Media Contacts:

| FRB: | Dave Skidmore | (202) 452-2955 |

| OCC: | Kevin Mukri | (202) 874-5770 |

| FDIC: | David Barr | (202) 898-6992 |

| OTS: | Erin Hickman | (202) 906-6677 |

| Year | Special Mention | Sub-standard | Doubtful | Loss | Total Classified | Total Criticized | Total Commitments | Total Outstanding |

|---|---|---|---|---|---|---|---|---|

| 1989 | 24.0 | 18.5 | 3.5 | 0.9 | 22.9 | 46.9 | 692 | 245 |

| 1990 | 43.1 | 50.8 | 5.8 | 1.8 | 58.4 | 101.5 | 769 | 321 |

| 1991 | 49.2 | 65.5 | 10.8 | 3.5 | 79.8 | 129.0 | 806 | 361 |

| 1992 | 50.4 | 56.4 | 12.8 | 3.3 | 72.5 | 122.9 | 798 | 357 |

| 1993 | 31.4 | 50.4 | 6.7 | 3.5 | 60.6 | 92.0 | 806 | 332 |

| 1994 | 31.5 | 31.1 | 2.7 | 2.3 | 36.1 | 67.6 | 893 | 298 |

| 1995 | 18.8 | 25.0 | 1.7 | 1.5 | 28.2 | 47.0 | 1,063 | 343 |

| 1996 | 16.8 | 23.1 | 2.6 | 1.4 | 27.1 | 43.9 | 1,200 | 372 |

| 1997 | 19.6 | 19.4 | 1.9 | 0.9 | 22.2 | 41.8 | 1,435 | 423 |

| 1998 | 22.8 | 17.6 | 3.5 | 0.9 | 22.0 | 44.8 | 1,759 | 562 |

| 1999 | 31.3 | 31.0 | 4.9 | 1.5 | 37.4 | 68.7 | 1,829 | 628 |

| 2000 | 36.3 | 47.9 | 10.7 | 4.7 | 63.3 | 99.6 | 1,951 | 705 |

| 2001 | 75.5 | 86.9 | 22.6 | 7.8 | 117.3 | 192.8 | 2,050 | 769 |

| 2002 | 79.0 | 112.0 | 26.1 | 19.1 | 157.1 | 236.0 | 1,871 | 692 |

| 2003 | 55.2 | 112.1 | 29.3 | 10.7 | 152.2 | 207.5 | 1,644 | 600 |

| 2004 | 32.8 | 55.1 | 12.5 | 6.4 | 74.0 | 106.8 | 1,545 | 500 |

(Dollars in Billions)

| Industry |

2004 | 2003 | 2002 | 2001 |

| Telecommunication & Cable |

||||

| Commitment |

120.2 |

149.7 |

174.1 |

197.5 |

| Classified |

13.1 |

35.7 |

38.1 |

6.9 |

| Special Mention |

10.8 |

7.0 |

9.0 |

10.0 |

| % Classified |

10.9% |

23.8% |

21.9% |

3.5% |

| % Special Mention |

9.0% |

4.7% |

5.1% |

5.0% |

| Manufacturing |

||||

| Commitment |

400.1 |

424.4 |

494.8 |

540.5 |

| Classified |

19.6 |

42.6 |

60.9 |

58.1 |

| Special Mention |

6.9 |

22.8 |

26.2 |

27.0 |

| % Classified |

4.9% |

10.0% |

12.3% |

10.8% |

| % Special Mention |

1.7% |

5.4% |

5.3% |

5.0% |

| Professional, Scientific, & Other Services |

||||

| Commitment |

107.3 |

122.4 |

124.9 |

157.9 |

| Classified |

3.3 |

6.8 |

8.8 |

11.9 |

| Special Mention |

1.1 |

1.8 |

2.3 |

4.5 |

| % Classified |

3.1% |

5.5% |

7.0% |

7.6% |

| % Special Mention |

1.0% |

1.5% |

1.9% |

2.8% |

| Oil, Gas, Pipeline & Utilities |

||||

| Commitment |

175.7 |

200.5 |

229.5 |

222.8 |

| Classified |

24.2 |

38.1 |

17.9 |

4.3 |

| Special Mention |

10.1 |

12.3 |

15.5 |

7.0 |

| % Classified |

13.8% |

19.0% |

7.4% |

1.9% |

| % Special Mention |

5.8% |

6.1% |

6.8% |

3.1% |

| Construction & Real Estate |

||||

| Commitment |

90.2 |

87.5 |

96.7 |

100.1 |

| Classified |

2.5 |

3.6 |

4.1 |

4.7 |

| Special Mention |

0.9 |

2.3 |

3.2 |

1.9 |

| % Classified |

2.8% |

4.1% |

4.2% |

4.7% |

| % Special Mention |

1.0% |

2.6% |

3.3% |

1.9% |

| Lodging & Transportation |

||||

| Commitment |

74.1 |

74.8 |

82.9 |

99.1 |

| Classified |

5.2 |

7.7 |

6.6 |

3.1 |

| Special Mention |

0.7 |

1.8 |

5.3 |

6.8 |

| % Classified |

7.1% |

10.3% |

7.9% |

3.1% |

| % Special Mention |

1.0% |

2.4% |

6.4% |

6.9% |

| Financial Services & Insurance |

||||

| Commitment |

337.1 |

343.3 |

376.5 |

420.8 |

| Classified |

2.1 |

6.7 |

8.9 |

11.9 |

| Special Mention |

0.5 |

2.5 |

2.9 |

4.5 |

| % Classified |

0.6% |

1.9% |

2.4% |

2.8% |

| % Special Mention |

0.2% |

0.7% |

0.8% |

1.1% |

| All Other |

||||

| Commitment |

240.5 |

241.0 |

291.6 |

310.9 |

| Classified |

3.8 |

11.0 |

12.7 |

16.3 |

| Special Mention |

1.8 |

4.7 |

14.6 |

13.9 |

| % Classified |

1.6% |

4.1% |

4.4% |

5.2% |

| % Special Mention |

0.7% |

2.0% |

5.0% |

4.5% |

| All Industries (Total) |

||||

| Commitment |

1,545.2 |

1,643.5 |

1,871.0 |

2,049.9 |

| Classified |

74.0 |

152.2 |

157.1 |

117.3 |

| Special Mention |

32.8 |

55.2 |

79.0 |

75.5 |

| % Classified |

4.8% |

9.3% |

8.4% |

5.7% |

| % Special Mention |

2.1% |

3.4% |

4.2% |

3.7% |

Footnotes

1. The Shared National Credit (SNC) Program was established in 1977 by the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency. In 2001 the Office of Thrift Supervision became an assisting agency. With a few exceptions, the annual program, which seeks to provide an efficient and consistent review and classification of large syndicated loans, generally covers loans or loan commitments of at least $20 million that are shared by three or more financial institutions. Return to text

2. Loan commitments included both drawn and undrawn portions of a loan or loan facility. Return to text

3. Excerpt from Federal Reserve's SR Letter 79-556 defining regulatory classifications: Classification ratings are defined as "Substandard," "Doubtful," and "Loss." A Substandard asset is inadequately protected by the current sound worth and paying capacity of the obligor or of the collateral pledged, if any. Assets so classified must have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt. They are characterized by the distinct possibility that the bank will sustain some loss if the deficiencies are not corrected. An asset classified as Doubtful has all the weakness inherent in one classified Substandard with the added characteristic that the weaknesses make the collection or liquidation in full, on the basis of currently existing facts, conditions, and values, highly questionable and improbable. Assets classified as Loss are considered uncollectible and of such little value that their continuance as bankable assets is not warranted. This classification does not mean that the asset has absolutely no recovery or salvage value, but rather it is not practical or desirable to defer writing off this basically worthless asset even though partial recovery may be effected in the future.

Excerpt from June 10, 1993 Interagency Statement on the Supervisory Definition of Special Mention

Assets:A Special Mention asset has potential weaknesses that deserve management's close attention. If left uncorrected, these potential weaknesses may result in deterioration of the repayment prospects for the asset or in the institution's credit position at some future date. Special Mention assets are not adversely classified and do not expose an institution to sufficient risk to warrant adverse classification. Return to text

4. Nonaccrual loans are defined for regulatory reporting purposes as "loans and lease financing receivables that are required to be reported on a nonaccrual basis because (a) they are maintained on a cash basis due to a deterioration in the financial position of the borrower, (b) payment in full of interest or principal is not expected, or (c) principal or interest has been in default for 90 days or longer, unless the obligation is both well secured and in the process of collection." In Table 1, nonaccrual classifieds are those funded or outstanding portions of loans classified as substandard and doubtful which are not accruing interest. For 2004, this consisted of $19.2 billion in loans rated substandard and $11.7 billion rated doubtful. Return to text

5. Note that the current industry totals categorizes borrowers using 2002 NAICS codes, in contrast to prior release of SNC data which categorized borrowers using 1997 NAICS codes. Return to text

6. Nonbanks include independent investment brokerages, investment vehicles, and other institutional investors. Return to text

7. For further guidance, institutions should refer to the July 12, 1999 Joint Interagency Letter to Financial Institutions on the allowance for loan losses, as well as the July 2, 2001 Interagency Policy Statement on Allowance for Loan and Lease Losses (ALLL) Methodologies and Documentation for Banks and Savings Institutions. Return to text

8. NAICS groupings of industries identified in Appendix B are as follows: Telecommunication & Cable - 5132 through 51339; Manufacturing - 31 through 33 and 5121 through 5131; Professional, Scientific, and Other Services - 54, 55, 56, 61, and 62; Oil, Gas, Pipelines, and Utilities - 21 (oil- & gas-related only), 22, and 486; Construction & Real Estate - 23 and 53; Lodging and Transportation - 48 (excluding 486), 49, and 72; Financial Services and Insurance - 52; and All Other - remaining NAICS codes. Prior year data has been restated to reflect industry categorizations using 2002 NAICS groupings rather than 1997 NAICS groupings used in prior data releases. Return to text